#10: Danahurt

EPS Recap, Bioprocessing Primer 2.0, Is Danaher Really a Long?

Introduction

I wanted to start off with a quick thank you to everyone who subscribed and/or responded to my prior article. I wish I’d started sooner, because what I’m about to write would have been even more timely just a week or two ago given how bioprocessing/Danaher earnings have gone so far.

Strap in, because I have another book report for you.

I published a primer on the bioprocessing space almost 2 years ago. Interestingly, while I hope it has proved valuable to others, it has also been valuable to me - I’d inadvertently made a have a time capsule into where my understanding of the space was in 2023 and where it felt short in helping me navigate the space in 2024.

While the fundamentals I laid forth in it remain true today, there are additional nuances that have been running in the background the entire time that I think are becoming important enough to talk about. This article builds on the original primer with a deeper look at the drivers of the biggest sources of revenue in bioprocessing.

While Danaher already took a beating over the last 2 weeks, I also try to frame the “not-long” case using the insights contained within, because one of the key takeaways is that not all bioprocessing exposure is created equal anymore.

Are We Off to a Good Start, or Not? Conflicting Tones to Start 2025

I published my Repligen thesis at the beginning of last week. The shortest version of the thesis was that there are so many company-specific tailwinds behind the business and its products in 2025 that I thought everyone should know about them before proceeding to even consider owning any other names in the space.

Tailwinds or not, however, the underlying market still needs to support the base, and some important cards have turned over since the beginning of last week.

We have now seen results from Sartorius, Lonza, Danaher, and Thermo Fisher, all key players in the bioprocessing ecosystem, as well as a handful of important softer read-throughs.

Unfortunately, so far these read-throughs fell short of providing the clarity investors crave, based on the conflicting stock reactions. That said, they did set the stage for improving clarity on how things are going over the next few months.

Sartorius: Great Q, if you can tolerate the weird “guidance”.

Sartorius’ 4Q was great across the board. Total revenue and EBITDA both beat, driven by strength in both segments. Somehow BPS revenue beating by 3% wasn’t the standout: it was the >20% beat in order intake, putting book-to-bill for bioprocessing at 1.18x. The only thing you could pick on was the refusal to give better than “moderate growth” as a tool to model 2025.

Management did say that it would grow “above industry” in bioprocessing, and that the normal market growth rate in bioprocessing is high-single-digits. They just wouldn’t tell us what “industry” means in 2025, only that it would be “lower”, without going into the components.

If you wanted to pick on something, it would have to be the guide - if orders were so great, why isn’t that lifting expectations?

The answer I’d propose to this is that the order beat was so large that one must assume that it had to come from a large enterprise-wide equipment order from a large customer. Sartorius hinted as much in the PR, but it’s important to be cognizant of how long it takes for some of these orders to turn into revenue. Management routinely tells investors that normalized lead times for consumables are 1-3 months, and that equipment falls in a much wider range of 6-18 months.

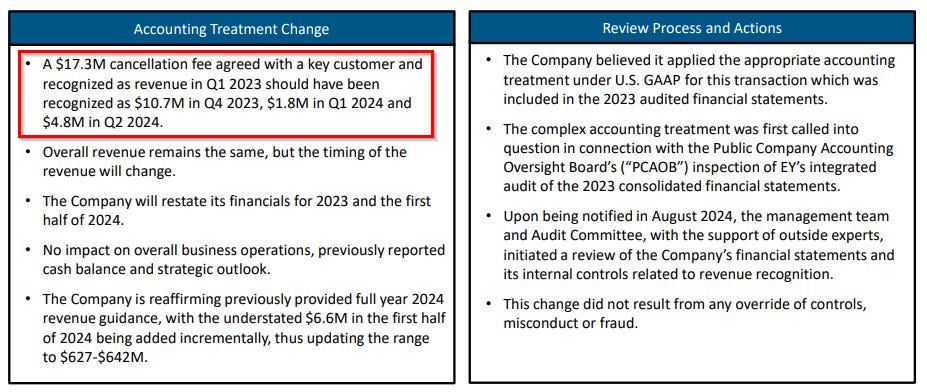

It’s not just Sartorius that has long lead times on equipment - some equipment is highly customized and part of customers’ long-term capex plans. I think Repligen’s accounting snafu last year illustrates this quite well:

The above is saying that Repligen got a sizable cancellation fee from a customer on an existing order - meaning it was likely placed sometime in 2022. It booked the fee in revenue when it was received, but later had to restate these numbers to reflect when delivery of orders took place. This moved revenues from 1Q23 to 4Q23 and 1H24. Even if you assume the order was placed just 1 quarter before cancellation, this is a 12-18-month lead time as well.

I suspect this is what is happening with Sartorius - a big 4Q win that benefits later periods that spills into 2026. While it takes away from the upside in 2025, it’s a still great signal - Sartorius has a big customer buying a lot of its stuff because it wants to make a lot of drug substance that will presumably turn into lots of consumable sales.

This is a razor-and-blade company with orders for lots of razors. Blades to follow.

Danaher: Sandbags or Sandstorm?

While Danaher gave rough numbers via pre-announcement at JPM, the real disappointment on its 4Q print was guidance. Consensus had total organic growth of ~5% and Danaher guided to 3%. When a stock trades at 31x forward EPS, you generally want the forward EPS to have upside, not downside, and you also want to see better than 3% organic growth - you can get that anywhere.

Given the moving parts, it’s best to show this guide in table form:

Looks pretty bleak - everything in both guides was below. In general I’m putting a little less weight on the 1Q25 surprise. Consensus numbers may be flimsy - the sell side doesn’t always roll out the quarters for year ahead until after the 4Q print, and those that do end up modeling on a 4Q that ends up coming in higher than guide, affecting the baseline. Danaher is also a notorious sandbagger when it comes to guidance anyway. If the FY deltas were as concerning as the quarter ahead, the stock would have been down another 10%.

For FY25, major drivers of the FY surprise were Biotechnology and Diagnostics. Life sciences was below as well, but it would have been reasonable to assume investors already saw the most downside potential there given all the uncertainty with the R&D market. The source of downside also came partially from an unexpected factor - Danaher’s remaining industrial exposure. Management also mentioned that Aldevron was tracking behind its deal model, which is unsurprising given the massive price tag relative to revenue at the time.

In Diagnostics, the guidance disappointment came from 1) weaker Cepheid respiratory sales estimates and 2) value-based-procurement headwinds affecting pricing in China. It’s worth pointing out that respiratory has seasonality that lands on the 4Q/1Q border, and Cepheid beat guide by $200M in 4Q in 2024.

The China update is annoying, but I’d take the respiratory guide with a positive grain of salt. Based on the past couple of years, it seems that for guidance purposes, management always assumes 1) seasonality it lands on the out-year 1Q part at the expense of the current year and that 2) if seasonality benefits the past 4Q, it must come out of the in-year 1Q. All else equal, this may have helped DHR set a bar they can beat here.

The component that some seem to disagree on is Biotechnology. I’ve seen it spun both ways. On one hand, order growth looked great, growing HSD% q/q again, +30% y/y. This could support the argument that guidance is just more sandbagging.

On the other hand, however, Danaher did belabor us with talk about exiting 4Q at a high-single-digit exit growth rate in bioprocessing, which most took to mean that next year could sustain that level. I see a two things undermining them here:

While q/q and y/y order growth looks great, comparable periods made growth easy to show for both.

The q/q comps have been artificially easy all year because customers have been gradually exiting phases of destocking.

Additionally, y/y comps are incredibly easy because Danaher allowed customers to cancel their orders, free of charge, in 2023, and they obliged.

The figure IR had tossed around was that “several hundred million” in cancellations took place between 2Q23 and 4Q23.

Assuming this conservatively means ~$400M, orders worth as much as 7% of bioprocessing (not biotechnology) sales were canceled in 3 quarters, which implies a ~10% growth headwind in the same quarters this year get lapped, before even considering demand growth comps.

It’s also worth pointing out that bioprocessing did worse than the broader Biotech segment in 4Q - at JPM, management stated that Discovery and Medical, which is ~20% of the segment, grew “double-digits”, which I took to mean some number above low-double-digits.

At 8.0% core growth for the Biotechnology segment in 4Q, this suggests that actual bioprocessing revenue only grew ~6.5% in 4Q.

Book-to-bill was only 1.0x, in the seasonally-beast quarter for bioprocessing orders.

With the above in mind, is a 1.0x book-to-bill on a weak revenue number really special? The outlook was still lower on a weaker performance in bioprocessing, even if growth rates end up where we wanted them to be.

Danaher also has a higher consumable mix than Sartorius, so the revenue trend itself is a stronger indicator of future revenue than it is over at the German counterpart.

Lonza: One Customer, But Upbeat & Investing Heavily

In the past 2 months, Lonza both hosted a Capital Markets Day and a fireside appearance at JPM. While management sounded energized about the road ahead at both, the story (and therefore the updates investors get) are a lot more about company-specific process at Lonza rather than the macro environment. The analyst day has great slides for those interested.

The print itself was overall neutral - Lonza ultimately missed 2H estimates by a touch, but guidance remained the same (presented at CMD). The one incremental tidbit, in my view, was that Lonza stated that it was seeing “positive developments” related to improving biotech funding.

Other Earnings Tidbits

The above companies have probably been the most important to pay attention to for bioprocessing, but there were a few tidbits in other prints worth taking note of:

Thermo Fisher shared last week that its 3% organic growth in Life Science Solutions was driven by Bioproduction and Biosciences.

Bioprocessing is <10% of Thermo’s sales, which implies just under half of the LSS segment, suggesting that ~40% of the segment is bioprocessing. If the rest were flat y/y, it’d suggest ~8% organic bioprocessing growth, arguably better than that of Danaher in 4Q.

IQVIA released results today, and suggested on its call that the strength in funding from last year was “starting to turn into RFPs” in real-time.

I’d see this as a slight disappointment, since these aren’t even bookings.

IQVIA also said pharma re-prioritizations are 70-75% complete. This means there are still some headwinds from additional spending cuts to chop through. There’s also no guarantee that new re-prioritizations don’t emerge

Steris also held its earnings call today. Steris is widely considered a medical device company, but some know that 20-25% of its AST segment is dedicated to bioprocessing, where Steris pre-sterilizes single-use bags and tubes before they reach a customer.

The company noted that bioprocessing demand was outpacing its own expectations, which supported the notion of a rebound. This was a change from its prior quarterly commentary.

So what gives? Some are more excited than others. I think I have some possible answers outlined later.

Have These Prints Changed Anything for Bioprocessing?

Short answer: no. At the risk of sounding conceited, these bioprocessing prints and read-throughs track fairly well with my views on the space. At the end of my last article, I hinted that I had a Danaher “short thesis” (if you could still call it that) in store for the future, while also saying that my best idea is a pure-play bioprocessing company. This only makes logical sense if I think that there are going to be winners and losers within the market, and this is indeed the case - I believe the landscape is shifting.

In articles past, I’ve claimed the following:

Bioprocessing is an oligopoly industry where suppliers enjoy the benefits of a regulatory moat that expands with economies of scale.

The bioprocessing market itself enjoys a stack of 2 secular growth trends (drug volumes and the shift to more complex molecules) that enable above-average, long-term growth.

Win rates are fairly consistent at the major players in the industry, allowing them all to partake equally in market growth. Customers tend to ensure that suppliers are actively competing with each other on new processes.

Differentiated growth comes from product-level exposure. Clinical exposure “outgrows” commercial because drug progression comes with large steps-up in volume demand, which repeats for several years when a drug goes commercial. Once commercial, growth is dictated by the aggregate of the drugs you sell into.

I am not doing an about-face on any of these. In the sections ahead, I do, however, want to walk through some of what I think is changing in real-time that investors should be aware of. A lot of these shifts are difficult to quantify, but I’m taking a couple stabs because no one else is trying.

One of the learnings of this exercise is that Danaher’s product portfolio may be uniquely exposed to the parts of the process that face headwinds resulting from these shifts. As such, I’m also going to lay out the short case for Danaher, which is really a “not long” case at this point, given how much of the valuation gap has closed vs peers.

I know the business is popular, so please don’t hate me if you’re among those who are faithfully long - the thesis is more about the external environment facing the company than the business itself the pain experienced post-earnings has left enough room for upside elsewhere to offset my base-case downside. My hope is that the thesis, even if partially post-mortem, comes across as a thought-provoking evaluation of risk many might have otherwise ignored.

I’ll back my sh*t up in the subsequent sections, but first, a refreshed look at the macro.